"A natural short position on housing"

Home ownership as risk avoidance

As governor of the Bank of Canada, Mark Carney gave a speech on Canadian housing in June 2011. Transcript. He explained why housing being scarce and expensive doesn’t benefit the economy as a whole:

The value of residential real estate holdings in Canada has climbed more than 250 per cent in the past 20 years, vastly outpacing increases in consumer prices and disposable income over that period. However, Canada is arguably no better off because of it. That’s because while homeowners may feel wealthier because of this rise in prices, housing is not net national wealth. Some Canadians are long housing; others are short.

The Economist explains this further in an article from April 2025:

You need to live somewhere. Until you own a place, you have a natural short position in property, because you need to inhabit one for the rest of your life (whether you rent or eventually buy).

Short positions are risky (who knows how far rents and prices might rise?). Buying a home closes the position, resulting in a neutral one; unlike other investments, it is not really a bet on where prices are headed.

Buying a home is one way to offset the risk of rising prices and rents. But in an expensive market like Vancouver, it has a lot of disadvantages compared to a financial investment like a low-cost index fund.

Disadvantages of real estate as an investment

When you invest by buying shares in a business, it’s because the business generates income, keeps some of it to expand the business (e.g. opening a new store or finding new customers), and pays out the rest to shareholders as dividends. Over the long term, you can expect capital gains, because the future income of the business should increase as it expands. By investing in a low-cost index fund, and thus spreading your investment over a wide range of businesses, you can avoid the risk of any one business or sector doing badly. By investing regularly, you can avoid the risk of putting all your money in when people are particularly optimistic and stock prices are at a peak.

When you invest by buying a home to live in, you get a steady stream of financial benefits, in the form of the rent that you don’t need to pay. But you’re completely undiversified - what happens if a big earthquake hits Vancouver? And you run the risk of buying in at the peak, as happened to investors in Toronto in the late 1980s: after inflation, prices didn’t recover for 20 years.

Alex Avery observes that over the 25 years from 1991 to 2016, a period when house prices rose as interest rates fell, the stock market outperformed housing. The average annual return on the S&P/TSX composite index was 8%, while the average annual return on Canadian house prices was 3.7%, after taking maintenance and transaction costs into account. That’s a 2.5X difference in total return over 25 years.

Summary of Alex Avery’s The Wealthy Renter (2016):

Homeowners aren’t usually aware of how much they’re paying for housing (Avery calls it “rent”). If you have a mortgage, you’re paying interest to the bank to “rent” their money; if your house is paid off, you’re paying the opportunity cost of having your equity tied up in your house instead of generating 4% annual income. As you pay down your mortgage, you’re shifting from one form of rent to the other.

As a result, homeowners tend to overconsume housing. For renters, it’s easier to see that your housing costs are pure consumption.

As an investment, housing has a number of other disadvantages. It’s illiquid, it’s not scalable (you can’t buy a fraction of a house), and it’s undiversified.

The big advantage of homeownership is that it’s a forced-savings program. So if you rent, you’ll want to do something equivalent to force yourself to save, using a payroll-deduction plan or automated monthly transfers to an investment account, and investing in something like VBAL or another asset-allocation fund with low costs.

The other interesting thing about The Wealthy Renter is that Avery examines specific housing markets: Toronto, Montreal, Vancouver, Calgary, Ottawa, and Edmonton. He concludes:

Among the six cities, Vancouver and Toronto offer the greatest cost savings to renters, with home ownership exceptionally expensive and house prices at extremely high levels. Calgary and Edmonton are more affordable but expose homeowners to the cyclical risk of energy-industry investment and employment, making renting a cheaper and lower-risk option. [He also points out the lack of land constraints in Calgary and Edmonton, limiting the prospects for price appreciation.]

Montreal and Ottawa offer the least risky home ownership options across these markets, with relatively stable markets, diversified employment, steady population growth, and house prices that are high by historical standards but relatively affordable compared to Vancouver and Toronto. Despite these lower risk profiles, in both Ottawa and Montreal renting is significantly cheaper than home ownership.

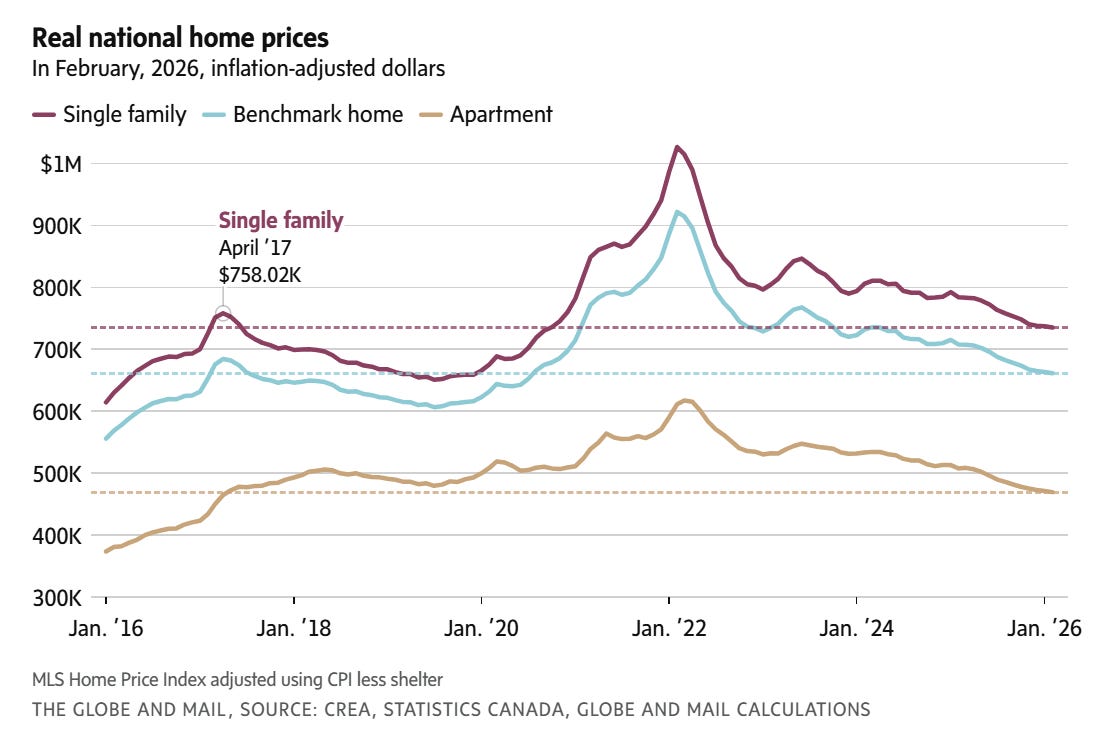

Average home prices, after inflation, are now where they were nine years ago. Canada inches closer to a lost decade for house prices after factoring in inflation. Jason Kirby, Globe and Mail.