Financing Growth: adjustments to Vancouver's up-front taxes

How does this affect the cost bottleneck?

2026 Financing Growth Update: Bill 16 Compliance Update to Density Bonus Provisions & Inclusionary Zoning. Staff report included on the agenda for today’s council meeting.

There’s two major bottlenecks to building the housing that we desperately need: the approval bottleneck and the cost bottleneck. (To paraphrase the MacPhail Report, we regulate new housing like it’s a nuclear power plant, and we tax it like it’s a gold mine.) This staff report is grappling with the cost bottleneck.

City review of up-front taxes on new housing

Council has a packed agenda over the next couple months, with both policy changes and individual projects.

City staff are currently working on a Financing Growth initiative, to address a fundamental challenge that Metro Vancouver municipalities face. With prices and rents slowly deflating, and with costs sharply up, municipalities can no longer extract $100,000 or so in cash and in-kind contributions from every new home. It’s basically killing the golden goose.

The BC government brought in legislation a couple years ago requiring municipalities to be more careful about their use of cash and in-kind requirements, with a deadline of June 30, 2026. Staff have written a report describing how they’re proposing to comply with the provincial legislation.

[My apologies to any OneCity members who are here because you’re voting in the nomination race this week. As the saying goes, you campaign in poetry; you govern in prose. Anyone who serves on city council is going to be dealing with a lot of prose! It takes a fair amount of work just to figure out what staff reports are saying. This report, which is only one of a number of staff reports on today’s agenda, is 100 pages.]

The report mostly deals with two policies: “density bonuses” and “inclusionary zoning.”

With “density bonuses,” a project pays to build more floor space, either in cash or as an in-kind contribution (e.g. building something and turning it over to the city). The city’s incentive is to keep the base zoning as low as possible.

“Inclusionary zoning” is more specific: it’s a requirement for a project to include a minimum proportion of affordable housing. A typical example is requiring a building to be 80% market and 20% non-market, with the 80% market side cross-subsidizing the 20% non-market side. My understanding is that this only ever worked for high-rises. It doesn’t work for a six-storey project.

Appendix F is a backgrounder on different variants of development charges. It never mentions the downside of development charges, which is that they ratchet up the floor on prices and rents for both new and existing housing. Or conversely, when prices have been slowly deflating, the cost of these policies has been pushing more and more projects underwater, as shown in this graphic.

What’s the report saying?

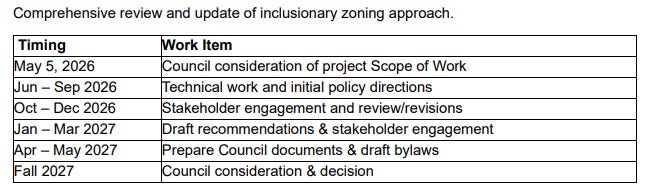

Today’s report is basically part one: comply with provincial legislation by June 30, 2026. There’ll be a second report towards the end of July 2026, to be approved after the election. Some of this work extends into 2027, well past the next election. From Appendix E, which describes the plan for inclusionary zoning:

One of the requirements of the provincial legislation is that the city needs to do a financial analysis of its inclusionary-zoning requirements. Appendix D is Coriolis’s analysis of the financial viability of the city’s inclusionary-zoning requirements.

The conclusion is that for west side lots that are at least 56 feet wide, when giving permission to build a multiplex (like a four-plex or six-plex) with 1.0 FSR, the city can extract a payment of about $27.50 per square foot, or $180,000 on a 56x120 lot. (Or the project can provide 5% of the floor space as “turnkey social housing” to the city, although this seems entirely pretextual - it’s hard to imagine a project actually doing this.)

For RM-8A zones (mostly in the Cambie Corridor area) where stacked townhouses are allowed at 1.2 FSR, on west side lots that are at least 56 feet wide, the city can similarly extract $44 per square foot, or about $350,000 on a 56x120 lot.

This is based on prices and costs in early 2026. If prices continue declining, or costs go up, the value that the city can extract without halting projects will go down.

The staff report is recommending three changes:

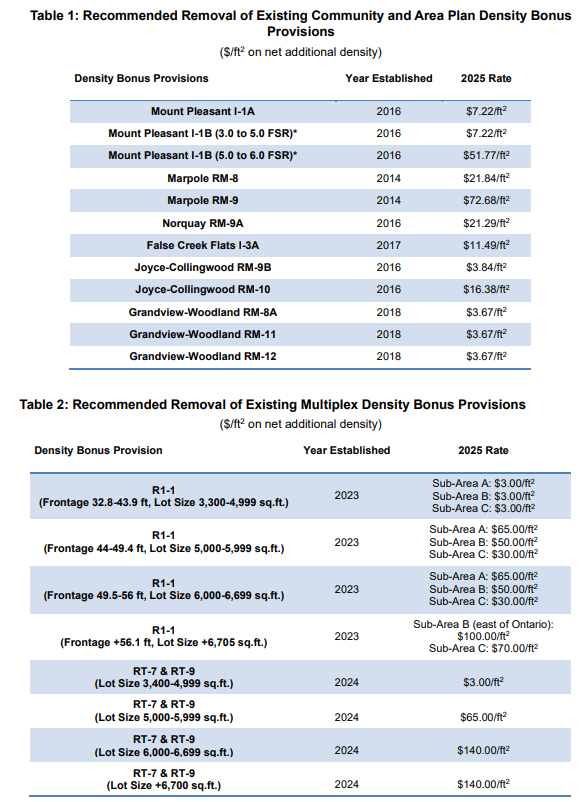

Remove density bonus requirements in the areas listed in Table 1 and Table 2, to be replaced with an Amenity Cost Charge specified in the July 2026 report. We don’t know yet what the ACC cost will be.

For large west side multiplex lots, charge $27.50 per square foot, and for large Cambie Corridor RM-8A (townhouse) lots, charge $44 per square foot. The economic analysis in Appendix D shows that this is viable.

For the zones in Table 3, we know that the requirements aren’t economically viable, but we don’t have time to fix them. We’ll fix them later.

I’m not sure why staff aren’t just recommending that these requirements be removed entirely, but … okay?

What does “not economically viable” mean?

From the staff report:

Economic testing indicates that some existing in-kind requirements are not currently viable and these will be reviewed and updated in Phase Two (see Appendix D for the economic testing of the inclusionary zoning recommendations). Phase Two will review and update Vancouver’s approach to inclusionary zoning and associated requirements to ensure the right balance between provision of needed affordable housing and project viability. Recommendations related to this will be brought to Council in fall 2027.

Appendix D analyzes each of the policies in Table 3. It’s quite funny, in a deadpan way. Basically, the amount of additional density needed in order for these projects to make sense is ludicrous.

4.7 IC-3A District - Apartment

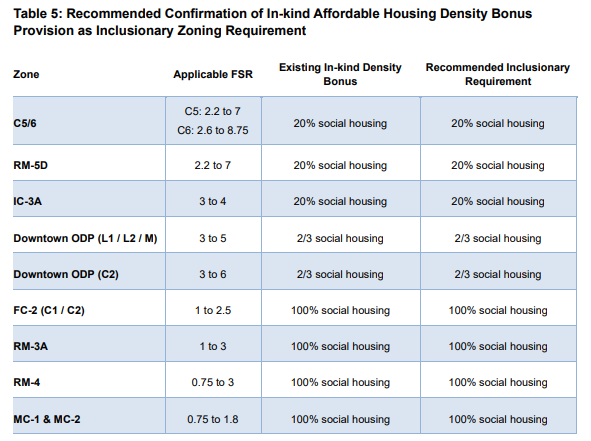

The base permitted density in the IC-3A District is currently 3.0 FSR. However, with bonus density, the IC-3A District allows mixed use strata apartment development up to 4.0 FSR if 20% of the residential floorspace is turnkey social housing.

The City is proposing to eliminate the density bonus for this option and implement inclusionary zoning.

Our financial analysis indicates that development is not financially viable at 4.0 FSR with a requirement for 20% turnkey social housing.

Therefore, the City asked us to estimate the density required to make it financially viable for projects in this zoning district to provide 20% turnkey social housing. We estimate that a total density of about 27 FSR would likely be required.

What does Appendix D say about each of these requirements?

C-6 and C-5A, 20% social housing: 8.75 FSR not viable, 13 FSR required.

RM-5D, 20% social housing: 7 FSR not viable, 18 FSR required.

IC-3A, 20% social housing: 4 FSR not viable, 27 FSR required.

Downtown ODP (L1), 2/3 social housing: 5 FSR not viable. “There is no density that would make this scenario financially viable.”

FC-2, RM-3A, RM-4, MC-1 and MC-2, 100% social housing: “There is no density that results in a financially viable project in the absence of government funding.”

Previously:

To come back to your earlier points about Solidarity - I can vibe with how these changes can help make alternative housing starts much more financially viable.

What's the carrot for existing homeowners? Most of them are locked into their fixed density homes, don't want their property tax mill rates to increase, and see the building of MORE housing (6-story or 20 story dwellings) as intrinsically detrimental to their future.

Very curious how quickly they move on any of these. We’re still in the permitting stage for 2 multiplexes, and these density bonus charges amount to 100k+ on each project.

The biggest issue with these charges is the bank won’t finance them up front, which increases the amount of up front capital you need to purchase the land + get the project to the construction stage.

Some nerdy financing math for a 4plx on the west side:

Land: 3 million

Total Construction: 3 million

Bank: ~4 million, with 1.5 million up front to help with land purchase

Equity: 2 million

The issue here is that you can’t draw from the construction loan to pay for the engineers, development charges, or bonus density fees that come up before starting the project. In this example, that amounts to over 500k (350k which is city fees), and you still need to pay to get the first 10% of actual construction done (250k) before you can draw on the loan.

What this means is you actually need is 2.25 million in equity to do the project (all contributed up front), which is ~10% more than the banks are calculating. This 10% gap forced us to back out of a recent project, as we couldn’t figure out how to get that last bit of equity. It’s a big reason why most applications right now are triplexes where the density charge is $3/ft instead of $65 (along with permitting time being twice as fast, which is another issue in and of itself).

One way to bring things in line is reducing the amenity charges (100k+ in this example with the $65 rate), the other is to allowed delayed payment until project completion for smaller builds like they’re doing with the larger ones.