The financialization diagnosis is wrong

The problem is scarcity: we want more rental buildings, not less

One diagnosis of the current housing crisis is financialization - the argument that prices and rents in Vancouver and the GTA are rising much faster than local incomes because institutional investors (“financialized investors”), like pension funds and Real Estate Investment Trusts, are buying up housing.

The Standing Committee on Human Resources, Skills and Social Development and the Status of Persons with Disabilities is studying financialization. The recently appointed federal housing advocate, Marie-Josee Houle, gave a presentation to the committee on May 9. The committee also invited the public to submit written briefs. I disagreed with Houle’s diagnosis of the problem, so I submitted a brief.

Scarcity

Intuitively, when prices and rents are rising much faster than local incomes, it’s natural to think that there must be outside players (foreign or institutional investors), not limited by local incomes, who are bidding up prices. Who else can afford it?

In fact, prices reflect scarcity, supply not keeping up with demand. In the case of housing, people don’t move around randomly - they move where the jobs are. In the GTA and Metro Vancouver, we have a mismatch between housing and jobs: we haven’t been adding homes fast enough to keep up with jobs. So prices and rents must rise to unbearable levels to force people to leave, matching those who remain with the limited supply.

We can see that the problem is scarcity by looking at rental vacancy rates, reported by CMHC every year. A healthy vacancy rate is 3%. When vacancy rates are closer to 1%, as they are in Metro Vancouver, people are having to squeeze into places that don’t really fit their needs, because that’s all they can find.

In Toronto and Vancouver, this is no longer just a problem for lower-income households. It affects anyone who’s not already a homeowner, especially younger people, all the way up the income scale, no matter how much money they make. A friend who used to work in operations management at a Vancouver hospital says that the last time they tried to hire an anesthesiologist, it took 18 months.

Housing is a ladder: it’s all connected. When there isn’t enough market housing being built, the people who would have lived there don’t vanish: they move down the housing ladder, to a place that’s smaller, older, or less secure, and bidding up rents on that rung. The result is trickle-down evictions, putting tremendous pressure on people near the bottom of the ladder.

In the last three years, the problem of scarcity has been greatly aggravated by Covid. Suddenly more people were working from home, and therefore needed more space.

Lack of purpose-built rental

The diagnosis of financialization being examined by the committee suggests that large institutional investors are the problem.

In Vancouver, multiple levels of government have been pushing in exactly the opposite direction. The problem here is that a lot of the rental market is in the form of condos and basement suites, rented out by an individual landlord, and these rentals provide very little security, because the landlord can always reclaim the suite for personal use. A survey by First United of recently evicted tenants found that more than half of the evictions were for this reason. Self-interest isn’t limited to corporations: when market rents are being driven up by scarcity, an individual landlord faces the same incentive to evict the current tenant and rent it at a much higher rate, or to sell to a new owner.

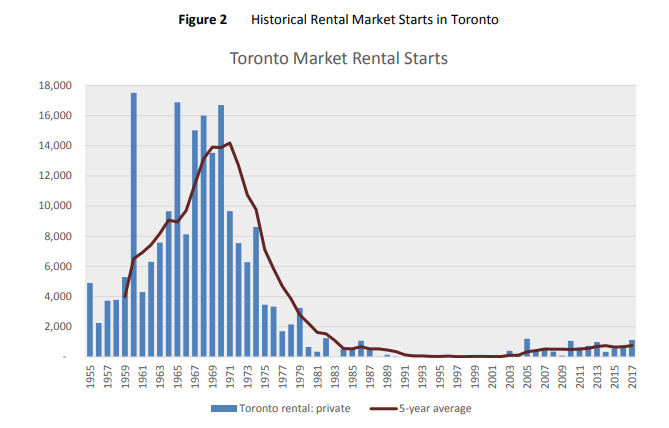

Thus in Vancouver, it looks like the problem is that we don’t have enough purpose-built rental buildings, built and operated by institutional investors such as pension funds and REITs, which need a steady long-term stream of income. There’s been few purpose-built rental projects for the last 40 years or so, because people are willing to pay more for a condo than a rental apartment (roughly 50% more). So a condo project will always be willing to pay more for the land (based on the expected value of the new building, minus all construction costs) than a rental project.

To offset this, the city of Vancouver has been allowing more density for rental buildings: providing a density bonus for a rental project that includes 20% non-market rentals, and allowing six-storey rental projects by right where four-storey condos are already allowed. The federal government is providing low-cost, long-term loans for rental projects through the Rental Construction Financing Initiative.

Suggested actions

To fix the housing crisis, we need to build more housing. I’d suggest that the overall direction of policy with respect to institutional investors should be to encourage them to build new rental housing, rather than acquiring and renovating existing rental housing - basically replacing older, cheaper housing with more expensive housing. (A comment from Peter Waldkirch, a director with Abundant Housing Vancouver: “Making it so that just about the only legal place to build a rental apartment is on top of an older apartment is dumb, cruel, terrible policy.”)

Acquiring older rentals. Along these lines, it seems reasonable to provide funding for non-profits to acquire and operate older rental buildings (basically like a non-profit REIT). They’ll need to go through due diligence to make sure that they’re getting it at a fair price, so they’re not surprised by unexpected costs for major repairs and renovations. This should be more cost-effective than building brand-new non-market housing. In BC, the provincial government has created a $500M fund for this purpose. If the federal government is able to contribute funding to an existing provincial initiative, that would be helpful.

RCFI. I’m sorry to disagree with the federal housing advocate, but the RCFI should continue. It’s a way to encourage more desperately needed rental housing, leveraging the power of the federal government to borrow money at a low rate of interest.

There’s been some discussion recently about increasing the affordability requirements of RCFI-funded projects. I would argue that its main focus should continue to be market rental housing. The RCFI provides an incentive to build rental housing instead of condos. It’d be reasonable to add an affordability requirement on top of that (e.g. 20% non-market) if it were possible to provide an accompanying density bonus, but that’s more appropriate for a municipal or provincial initiative.

Taxes and charges. Taxes on new housing work the same way as the carbon tax - if you increase taxes on something, you get less of it. The federal government should be paying attention to taxes and charges on new housing, especially those under its direct control: given the desperate need for more housing, CMHC recently increasing its insurance premiums on rental construction loans seems counter-productive.

Permission timelines and Infrastructure funding. To build new housing, you need permission. A significant issue identified by the MacPhail Report (the joint federal-provincial expert panel on housing supply in BC) is that it’s extremely slow and difficult to get municipal approval to build new housing, for both market and non-market projects. This is tied to municipal development charges and to infrastructure upgrades (such as sewers). The federal government can help with infrastructure funding, through the Housing Accelerator Fund - basically “allow more housing, and we’ll give you funding to upgrade infrastructure.”

More

Transcript of May 9 presentation by Marie-Josee Houle, federal housing advocate.

Video of May 16 meeting - the transcript isn’t posted yet.

First United eviction survey, May 2023.

The financialization of Canadian multi-family rental housing: From trailer to tower. Martine August, February 2020. Presents the argument that acquisition of rental housing by large corporate landlords is what's driving up rents. (I would argue that corporate landlords evicting tenants and raising rents is a symptom of scarcity. Scarcity results in a huge and increasing gap between market rents and actual rents, and this gap means there's similar incentives for individual landlords to evict tenants or sell.)

Toward Evidence Based Policy: Assessing the CMHC Rental Housing Finance Initiative (RCFI). Steve Pomeroy, January 2021. Probably the most prominent project receiving RCFI funding (this reducing financing costs) is Senakw.

Herle Burly podcast episode: housing panel with Mike Moffatt, Diana Petramala, Adam Vaughan, and Mukhtar Latif, April 2022. I follow Mike Moffatt pretty closely - he provides a lot of evidence that housing scarcity is what’s driving up prices in Ontario. If I understand correctly, Adam Vaughan believes that financialization is an alternative explanation.

Previous posts: Bottlenecks to new housing, including economic viability. BC to acquire older, cheaper rentals. Tax increases on new housing are bad. The MacPhail Report.