What the cost bottleneck looks like

Every cost increase takes a bite out of the apple

There’s three bottlenecks to building more housing:

The approval bottleneck (“it’s easier to elect a pope”)

The cost bottleneck: what’s the value of the new building, minus the total cost to build it?

Physical construction

What does the cost bottleneck look like? Here’s a simple example, based on an March 2023 example from Coriolis. It’s a hypothetical project that’s replacing four single-detached houses with a six-storey condo building, with 45 apartments.

Total: Start with the estimated value of the new building. In this example, it’s $1257 per buildable square foot.

Subtract all the costs of building it (shown in red): $1011 per buildable.

The resulting land value is $268 per buildable square foot. We can divide it into $205 per buildable (the current value of the land with its existing buildings, shown in blue) and $63 per buildable in “land lift” (shown in green).

Land lift is the premium that landowners get when they sell, compared to the current land value. In this example it’s about a 30% premium ($560,000 on top of the current $1.8M land value for each lot).

When there’s a lot of land lift, with high prices and low construction costs, you can expect to see a lot of development, because landowners will be willing to sell. When there’s little or no land lift, nothing happens.

Coriolis suggests that the city can charge a Community Amenity Contribution of $32 per buildable (shown in yellow), leaving $31 per buildable (about $270,000, or a 15% premium) for the landowners. 15% seems like it might not be enough: elsewhere Coriolis suggests 20% as a rule of thumb.

The original numbers in the example are shown below. Scenario 1 (which isn’t economically viable) is omitted. I’m assuming the four lots are 33 x 122, that the allowable floor space is 2.2 FSR, and efficiency (after subtracting space for hallways, stairs, and elevators) is 85%, resulting in an average apartment size of about 670 square feet.

Without land lift, nothing happens

Land lift is critical. If the new building minus the cost to build it is less than the current value of its property, as in Scenario 1, then the project doesn’t make sense, and it won’t happen.

If there’s an increase but it’s too small, it won’t happen either: the landowner isn’t likely to sell unless the land lift is significant. Michael Manville explains:

The typical landowner is a satisficer, right? They're not someone who needs to make the absolute most money possible out of their property, they're someone who is fine making a comfortable amount of money at minimal effort. And in property markets and land markets, like Los Angeles, Seattle, Boston, and so forth, owning land is just a pretty good gig. And you can be doing almost nothing and making quite a bit of money. And so, to have someone come to you with the prospect of making more money, if you go through all the hoops that are involved in property development, that end result of more money has to be really big, to change that inertia.

Too many bites out of the apple

The city aims to maximize its CAC revenue by taking as much of the land lift as it can - usually about 75-80% of it, leaving only 20-25% to motivate landowners to sell.

The problem is, selling prices and construction costs are always changing. Because the land value is only about 20-25% of the total project cost, a small change in either price or construction cost will have an outsized effect on land value: for example, if land value is 20% of the total project cost, and construction costs rise by 10%, then land value will decrease by about 40%.

In the last couple of years, the economy has been overheating (people were spending a lot more time at home during Covid and wanted more space), resulting in higher prices for both labour and materials. The Bank of Canada has raised interest rates sharply to cool down the economy, resulting in both lower prices and higher borrowing costs.

Costs are cumulative: they add up. Any increase in labour and material costs, permit fees, development charges (like the Metro Vancouver DCCs), or borrowing costs makes it more difficult for projects to happen.

(This is why the federal government removed the GST from new rental housing, as recommended by the National Housing Accord: it reduces costs for rental projects. It’s expected to result in 200,000 to 300,000 more rental units getting built over 10 years.)

When land lift is gone, projects wait for higher prices and rents

Who pays for increased costs? Is it the landowner (since the developer can pay less for land), the developer (who has to accept reduced profit), or the homebuyer (who pays a higher price)?

When there’s a lot of land lift, costs come out of land lift and are borne by the landowner. Minjee Kim:

Project feasibility for multifamily commercial developers probably isn’t impacted too much by the higher exaction standards. These developers will essentially say that as long as the rules are stated clearly upfront, and they can expect how much they need to factor in, in their pro forma, this is okay because they're essentially going to pay less for developable sites.

But what happens when the land lift is gone?

Developers need a minimum rate of return (profit), typically 15% for condo projects and 10% for rental projects, in order for projects to make sense. Without this level of profit, they won’t be able to get construction loans, for example.

So when projects aren’t economically viable at current prices and rents, what happens is that they have to wait until prices and rents go up, resulting in more land lift. In other words, it’s homebuyers and renters who end up paying for the increased costs.

An example from the Broadway Plan:

In this case, the 20% below-market requirement is basically a tax on new housing, except that it's in-kind instead of cash. The city's economic testing shows that in order to pay for the 20% below-market rental from land lift, the project would need 10-15 FSR. Instead, they're limiting projects to 7.5 FSR, or lower in a lot of neighbourhoods. Which means that rents will need to rise significantly in order to pay for the 20% below-market rental. The cost of the 20% below-market rentals is being passed through to market renters.

A self-fulfilling prophecy

One other aspect of the city’s attempt to maximize CAC revenue is that the city asks for CAC fees based on the maximum possible selling price. But then that’s a self-fulfilling prophecy: a project which pays those fees must sell at that price in order to be economically viable. As Michael Mortensen puts it, prices ratchet upwards. The city doesn’t have any incentive to look at projects which sold for lower prices when setting their CAC targets.

As the MacPhail Report points out, the CAC revenue-maximizing process means that the incentives for the city are backwards. Instead of aiming to reduce costs, the city is aiming to set them as high as possible.

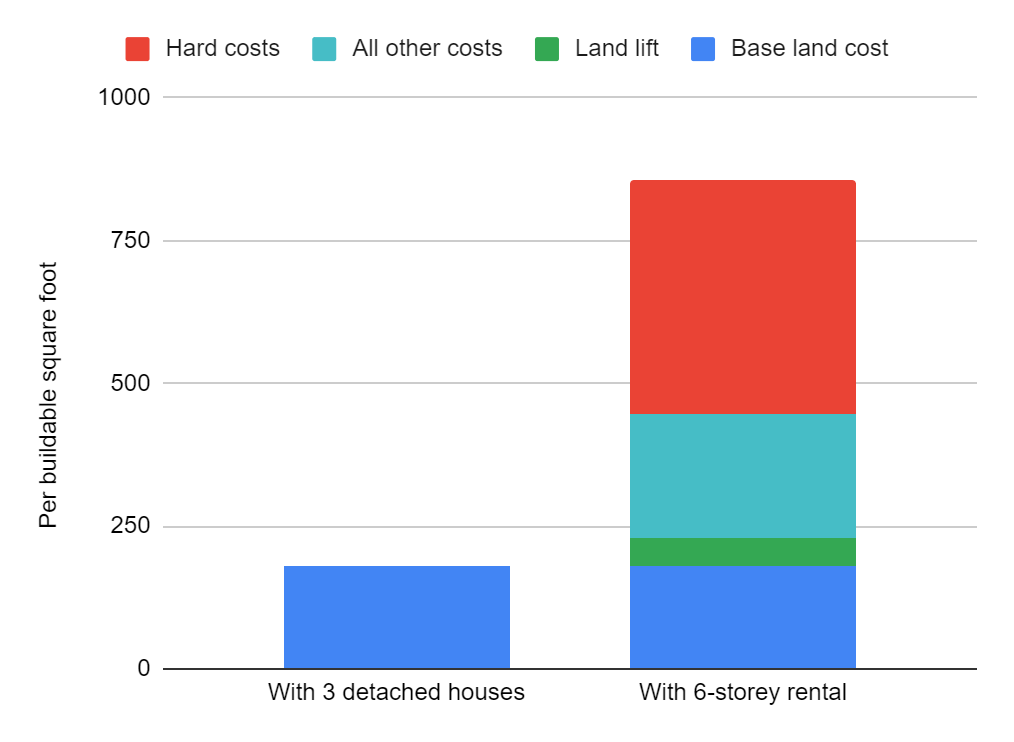

A six-storey rental example

Another example, based on a May 2022 analysis from Coriolis. It’s a six-storey, 70-unit purpose-built rental building in the Broadway Plan area, replacing single-detached houses on three 50-foot lots.

Total: The estimated value of the 6-storey rental building for the future owner, based on current rents and a 4.2% annual yield. (This is comparable to a GIC: owning a purpose-built rental is a low-risk, low-return business, which is why pension funds and REITs own them.) In this example, it’s $857 per buildable square foot. (People are willing to pay roughly 50% more for condos compared to rental apartments.)

Subtract labour and materials (red), called “hard costs.” $411 per buildable square foot.

Subtract all other costs (turquoise), including 10% profit for the developer. (For condos it’s 15%.) $216 per buildable square foot.

The resulting land value is $231 per buildable square foot. Coriolis suggests that the premium over the existing value would need to be about 20%, suggesting that the existing value is $180 per buildable, and the land lift is $50 per buildable.

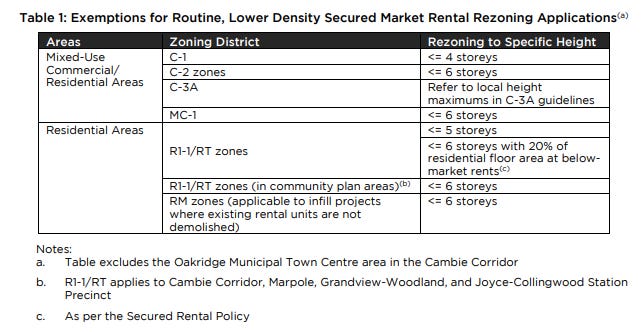

Note that certain low- and mid-rise rental projects aren’t subject to CAC negotiations. Purpose-built rental housing, which provides more security than renting a condo, is considered to be a public amenity in itself. The Goodman Report blog quotes the city’s CAC policy:

It is recommended that the CAC process be streamlined so that routine, lower density rental rezoning applications (outside the Downtown) be exempt from CACs. This approach would enable a majority of rental rezoning projects to proceed without a CAC and free rezoning applications from participating in the City’s negotiated CAC process while also having the added benefit of allowing staff more time to work on complex, larger rezoning applications.

The specific exemptions:

It appears that other purpose-built rental projects still need to go through the CAC process.